Waiting for Rates in the 5s? Here’s Why That Might Not Matter as Much as You Think

Mortgage rates already dipped into the upper 5s twice this year… and both times, they didn’t stay there long. A few days later, they bounced right back into the low 6s.

And if you saw that and thought, great, I missed it, trust me, you’re not alone.

A lot of buyers are acting like the 5s are some kind of golden ticket. Like the second a rate starts with a 5 instead of a 6, everything magically becomes affordable again. And emotionally? Sure, it feels huge.

But financially? The difference may be a whole lot smaller than people think.

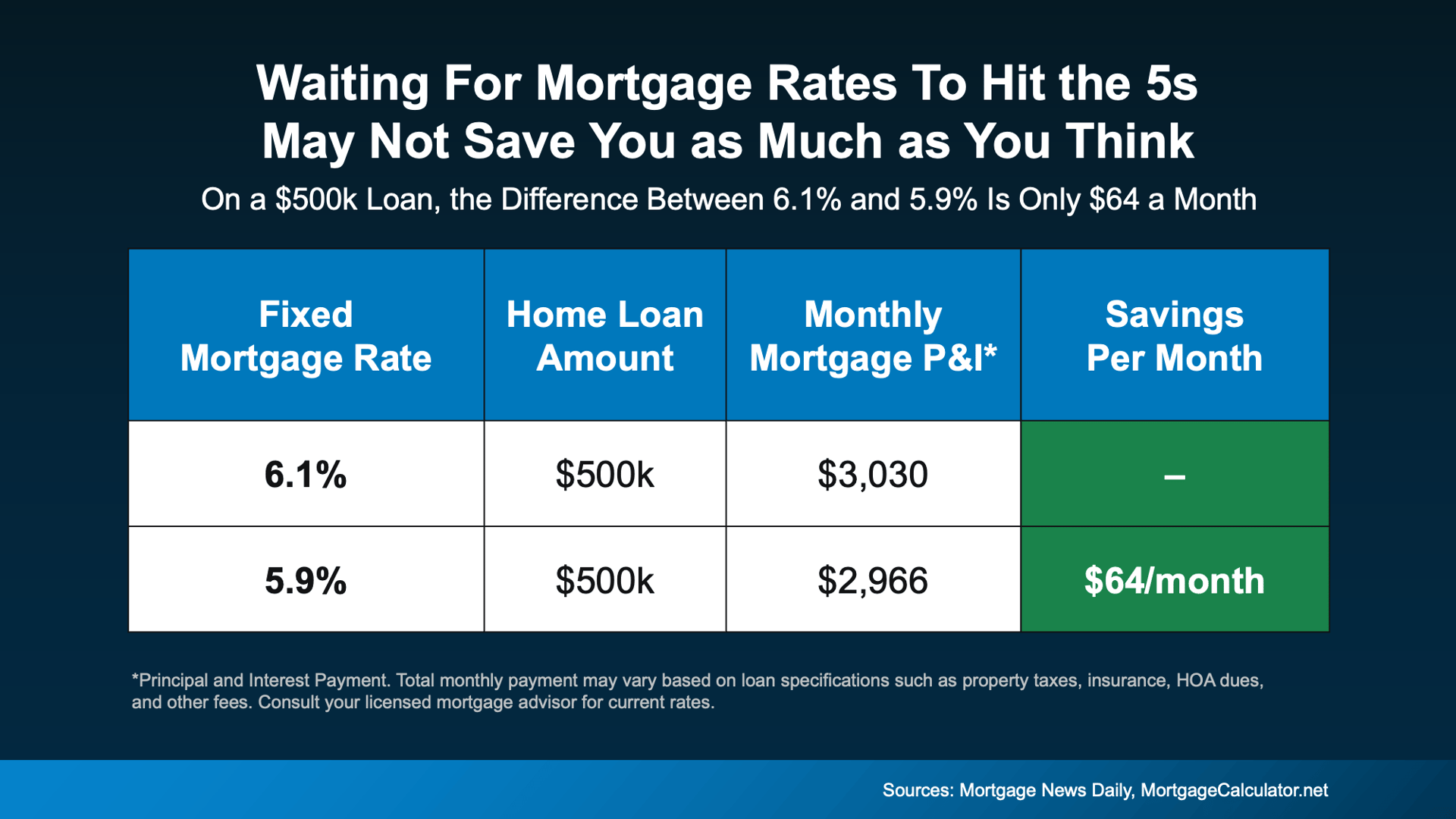

The monthly payment difference is not exactly life changing

Let’s break it down.

On a $500,000 loan, a rate of 6.1% gives you a principal and interest payment of about $3,030/month. At 5.9%, that payment drops to around $2,966/month.

That’s a difference of about $64 a month.

Not $300.

Not $500.

Just $64.

Yes, that adds up over time. Of course it does. But for many buyers, it’s not the dramatic drop they’ve built up in their heads while waiting for “the perfect rate.”

Sometimes the idea of getting into the 5s feels bigger than the actual payment relief.

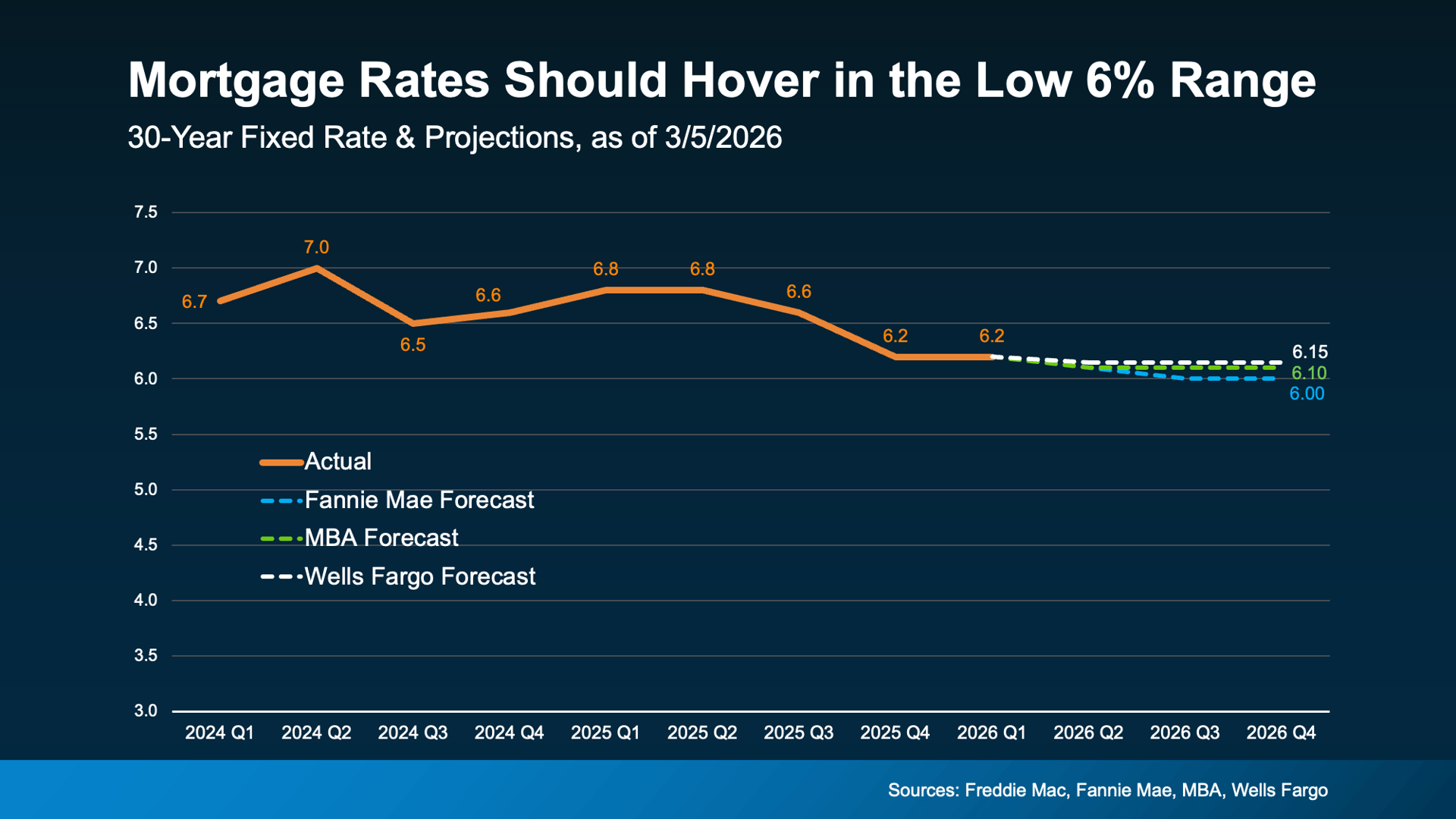

The experts are not calling for a major rate plunge

Here’s the other piece buyers need to hear: most housing economists are not predicting some big, lasting return to super-low rates anytime soon.

Will mortgage rates bounce around a bit? Absolutely. Could they touch the high 5s again here and there? Sure.

But the general expectation this year is that rates stay closer to the low 6% range, not camp out in the 5s for the long haul.

So if your whole strategy is built around waiting for some dramatic drop, you may be waiting a long time for a reward that doesn’t move the needle nearly as much as you hoped.

The better question is not “Did I miss it?”

The better question is:

Does today’s payment work for me?

Because that’s really what matters.

If the payment is comfortable, the home fits your needs, and the timing is right for your life, the difference between 6.1% and 5.9% probably is not the thing that should make or break your decision.

And let’s not forget — a mortgage rate is not forever.

If rates come down in a meaningful way later on, you can always refinance. But you cannot refinance a home you never bought.

Waiting can feel safe… but that does not always make it smart

It makes total sense to want the best rate possible. Everyone wants the best deal. But sometimes buyers get so focused on chasing a number that they miss the bigger picture.

Rates have already improved from where they were. Not long ago, buyers were looking at rates in the 7s. Now we’re hovering in the low 6s.

That drop already changes affordability more than many people realize.

So before you decide your window has closed, run the numbers again. Take a fresh look. You may find that the opportunity did not disappear at all — it just looks a little different than you expected.

Bottom line

If you’ve been waiting on the sidelines for some magic number on mortgage rates, it may be time to rethink the strategy.

Because the difference between the high 5s and low 6s may be a lot smaller than it sounds.

And the right move is not always about chasing the lowest possible rate. It’s about knowing when the numbers, the home, and your goals all line up.