The Fed Doesn’t Directly Set Mortgage Rates

Right now, everyone’s watching the Fed. Most economists expect a cut to the Federal Funds Rate at their mid-September meeting to help keep a cooling economy from slipping into a recession.

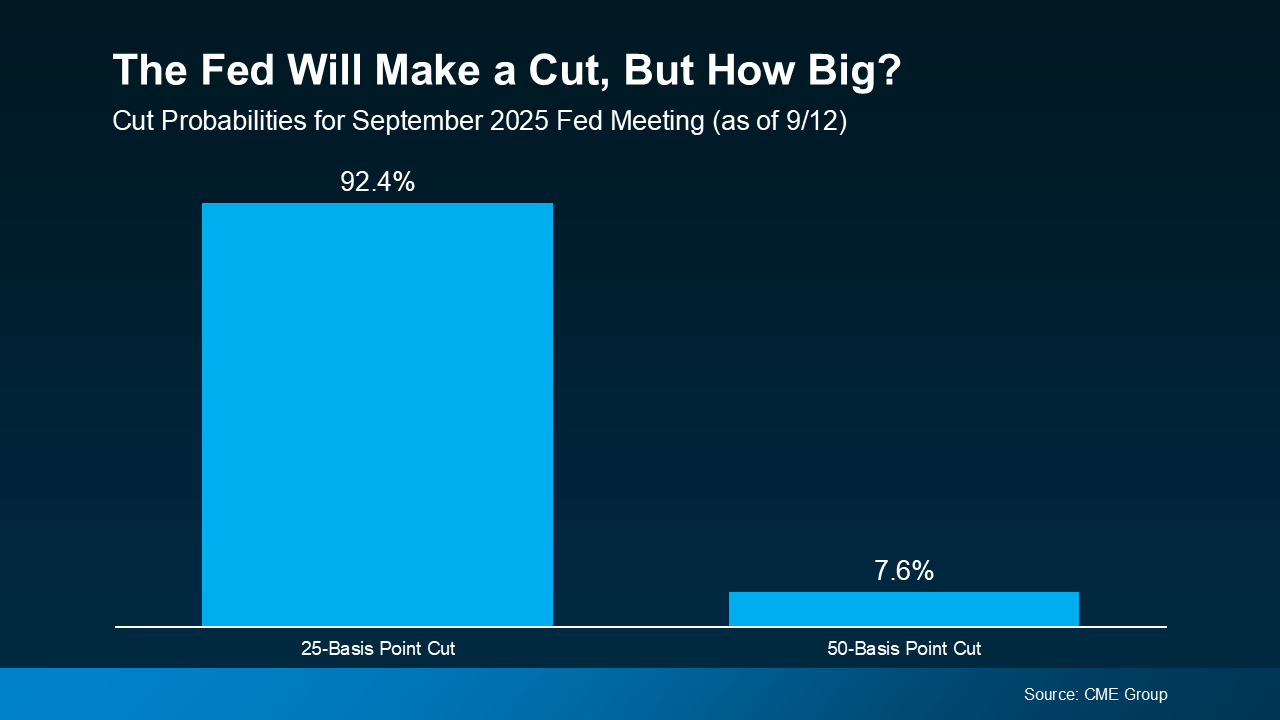

Markets are already ahead of the game. According to the CME FedWatch Tool, there’s virtually a 100% chance of a September cut. The odds favor a small cut (25 basis points), but there’s still a chance of a larger 50-basis-point move.

What the Federal Funds Rate Really Is

The Federal Funds Rate is the short-term interest rate banks charge each other. It influences borrowing costs across the economy — but it’s not the same thing as mortgage rates. Still, the Fed’s decisions can set the tone for where mortgage rates head next.

Why Markets Moved Before the Fed Did

Here’s the surprising part: mortgage rates tend to respond to what markets expect the Fed will do, not just what the Fed actually announces. When traders think a cut is coming, that expectation gets priced into mortgage rates ahead of time.

That’s exactly what happened after weaker-than-expected jobs reports on August 1 and September 5. Mortgage rates dipped as confidence in a Fed cut grew. Even with a slight uptick in the latest CPI inflation report, markets still expect a cut.

If the Fed sticks with a 25-basis-point cut, that’s likely already baked into today’s mortgage rates. But if they go bigger — 50 basis points — rates could slide more than they already have.

Where Mortgage Rates Could Go Next

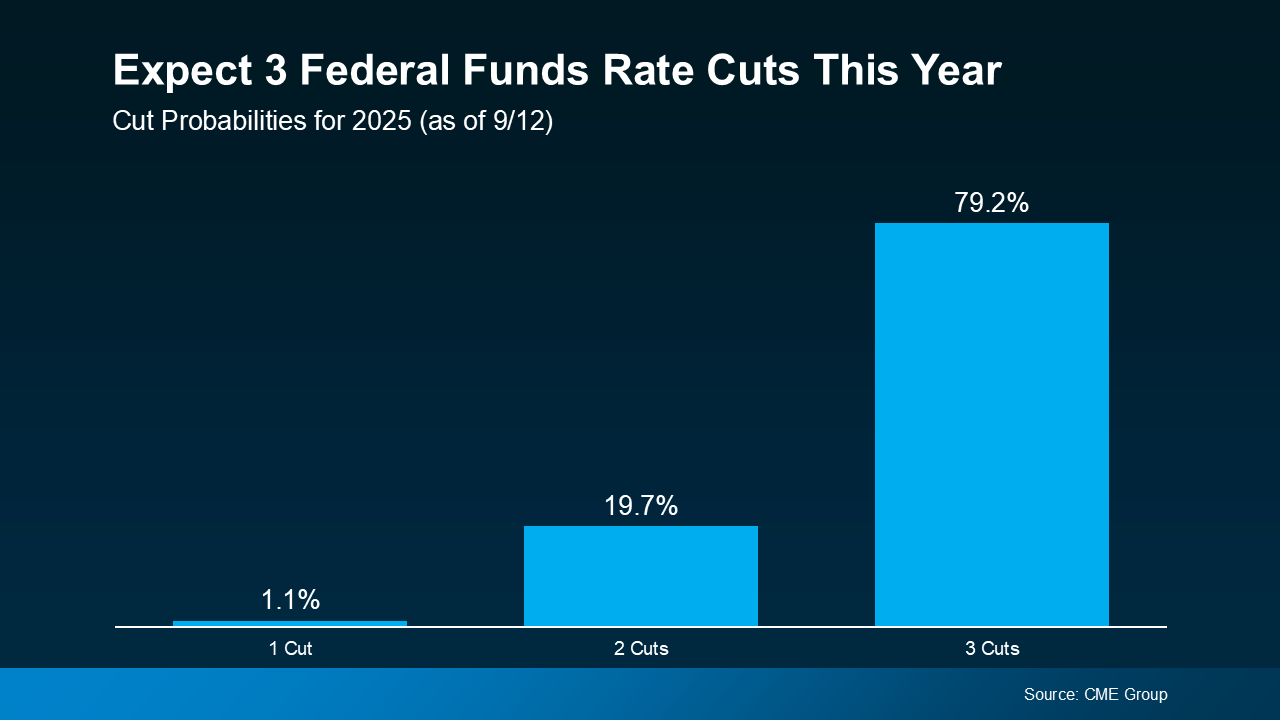

This first cut might not move the needle much. But many experts think the Fed could trim rates again before year-end if the economy keeps cooling (see graph below).

Sam Williamson, Senior Economist at First American, puts it this way:

“For mortgage rates, investor confidence in a forthcoming rate-cutting cycle could help push borrowing costs lower in the back half of 2025, offering some relief to housing affordability and potentially helping to boost buyer demand and overall market activity.”

If multiple cuts happen — or even if markets simply believe they will — mortgage rates could ease further in the months ahead. But there’s a catch: unexpected inflation spikes or other surprises could quickly change the outlook.

Bottom Line

Mortgage rates won’t drop overnight, and they don’t move one-for-one with the Fed’s decisions. But if a true rate-cutting cycle takes shape and markets stay convinced, we could see lower mortgage rates later this year and into 2026.

If you’ve been waiting on the sidelines, now’s the time to talk strategy. Even small changes in rates can make a big difference in affordability — and knowing what’s ahead can help you make the smartest move for your situation.