Still Clinging to That 3% Mortgage? Let’s Talk.

We get it. If you locked in a mortgage rate around 3%, giving that up probably feels like a huge financial step. And even if the idea of moving has crossed your mind, there’s that little voice in your head saying, “Why would I give that up?”

But here’s something we see a lot: when you focus too much on the rate, you might be ignoring the bigger picture—your life.

Most people don’t move because of interest rates. They move because life changes. So instead of asking why you’d give up your rate, let’s ask this instead:

Will you still be living in your current home five years from now?

Take a second and really think about that. Are you planning on expanding your family? Downsizing now that the kids are out of the house? Eyeing retirement or looking for more space to work from home?

If you truly love where you are and nothing big is going to change, then staying might make perfect sense. But if there’s even a slight chance you’ll want or need to move, even a few years from now, it’s time to start thinking about timing.

Because waiting even a year or two could make a big difference in what your next home will cost.

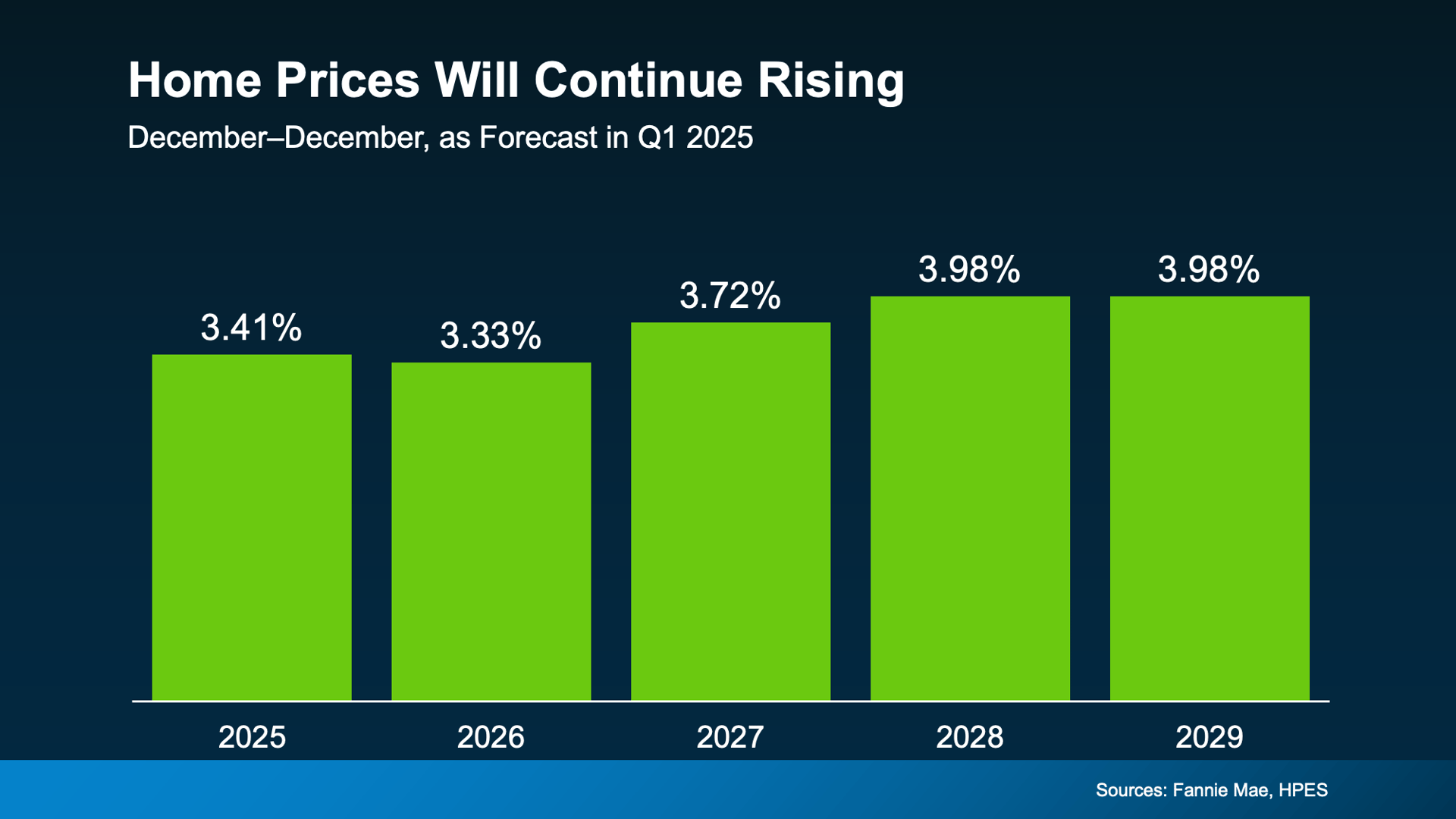

What Experts Are Saying About Home Prices Over the Next 5 Years

Fannie Mae surveys over 100 real estate experts every quarter to get a sense of where home prices are headed. And the message is clear: prices are expected to climb steadily through at least 2029.

(See graph below)

These projections aren’t showing wild spikes, but steady growth adds up fast over time. Sure, some local markets may see flat or slower growth here and there, but historically? Home prices go up over the long term.

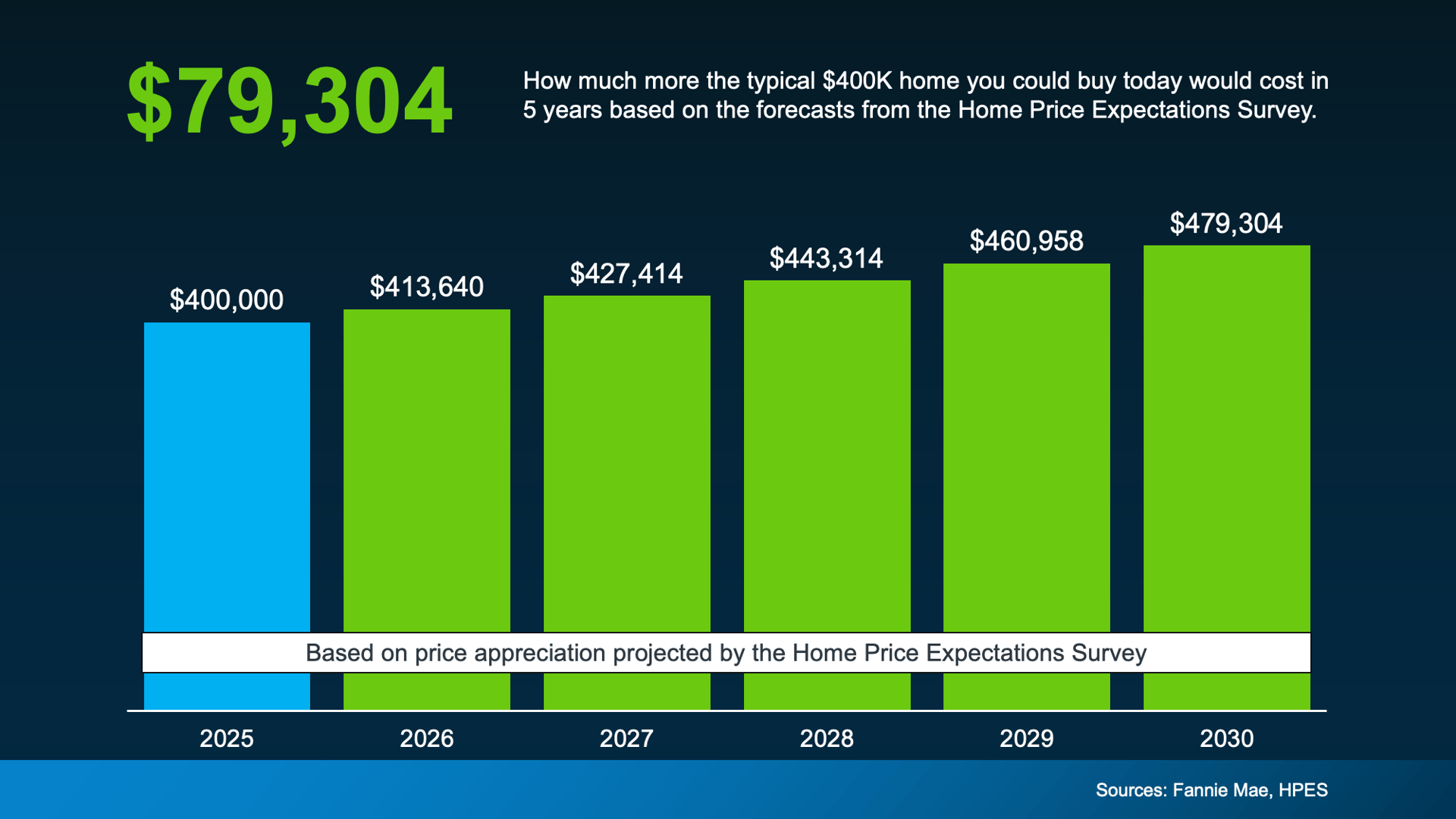

Let’s put it into perspective. Say you’re thinking about buying a $400,000 home in the future. Based on these expert forecasts, waiting five years could mean paying nearly $80,000 more.

(See graph below)

That’s a big jump—and that’s just the price. Add in rising insurance costs, property taxes, and repairs on your current home as it ages, and suddenly waiting doesn’t feel like the money-saving move it once did.

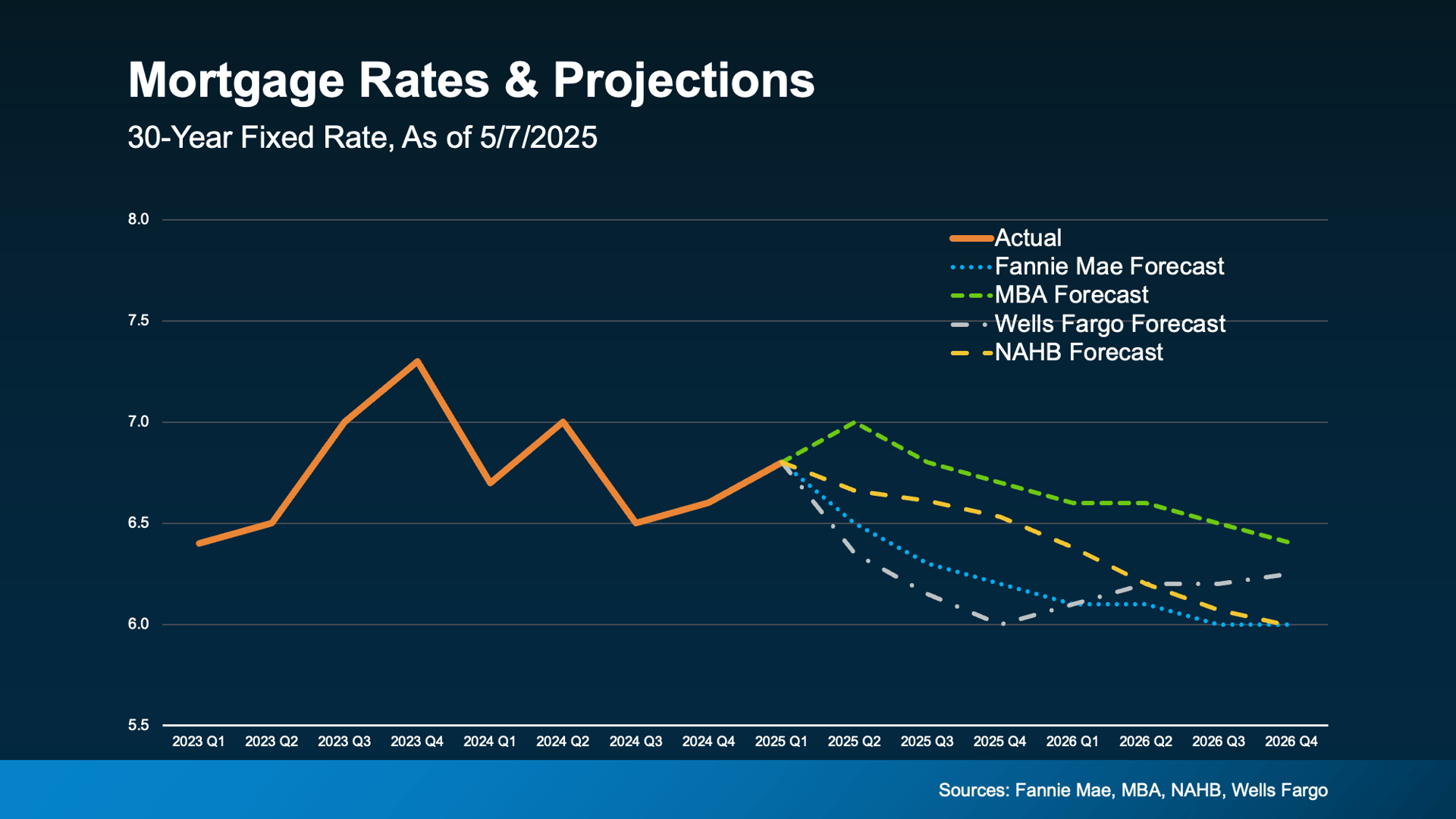

What About Interest Rates?

We know you’re probably waiting for that magical 3% rate to come back around. But experts agree: that ship has sailed. Even if rates do come down a bit, we’re just not expected to return to pandemic-era lows.

(See graph below)

So maybe the question isn't “why would I move?” It’s actually “when should I?”

And when you look at the numbers, you might find that waiting isn't actually saving you anything.

Bottom Line

That low rate served you well—but if it's holding you back from making a move that fits your life today, it might be time to reassess.

If a move is even somewhat on your radar, now is the perfect time to run the numbers together. We’ll walk you through how future price increases could impact your plans, and what options make sense for you—whether it’s six months or six years away.

Curious what the numbers look like for a $500K home? Or $900K? Let us know, and we’ll crunch the math. No pressure—just smart planning.